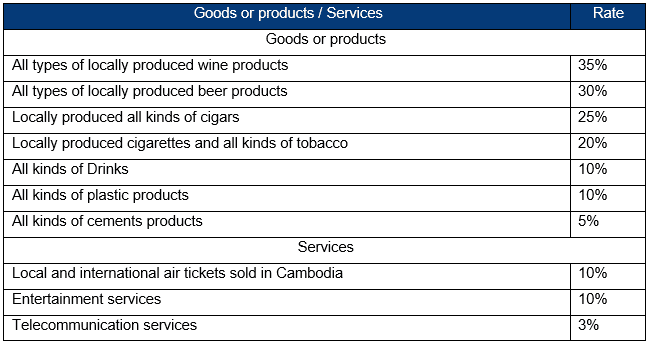

SPT is a monthly tax that is imposed on some locally produced and imported products and services. The local taxpayer producing or supplying these merchandises or services is responsible for paying this tax.

Tax Rate

*Term “Entertainment services” included concerts, music, soundtracks, stage show, massage, steam, sauna, car racing, motor racing, snooker, bowling, all games and hockey.

*Note: In contrast to the public lighting tax, which is paid at all stages of the supply, the Special Tax is paid only once by the producer or importer

Tax Calculation Based

*For local products: 90% of selling price exclude its SPT, PLT and VAT.

*For services: 100% of selling price exclude its SPT, PLT and VAT.

Tax Exemption

The following goods or products are exempted:

unprocessed tobacco and wine

Sour palm juice

Mineral water

Fruit nectar

Fresh vegetables

Ice cream

Lotus nuts

Milk drinks

other services instead

Using Invoices

Medium and large taxpayers must keep invoices for at least 10 years, and small taxpayers are at least 3 years.

Accommodation Tax (ACCT)

Accommodation Tax is a monthly tax that is imposed on the supply of accommodation services at a rate of 2% of the taxable value inclusive of all taxes except ACCT and VAT.