*A Cambodian resident taxpayer’s worldwide salary (Cambodian and Foreign sources) will be subject to Cambodian Tax on Salary.

*For non-residents, only the Cambodian-sourced salary will be subject to Tax on Salary.

Residency and non-residency

*A Cambodian resident taxpayer includes any physical person who:

has a residence in Cambodia;

has a principal place of abode in Cambodia; or

is physically present in Cambodia for more than 182 days in any 12-month period ending in the current tax year.

*A non-resident for tax purposes is any person who is not a resident in contrast with the above criteria.

Tax On Salary Based

The following payments are included to be the base for calculating tax on salary:

Basic salary

Year-end bonus/ bonus

Overtime/ hardship compensation

Loan to staff

Advance salary

Seniority (not allowed by law)

Commission

Other incentives

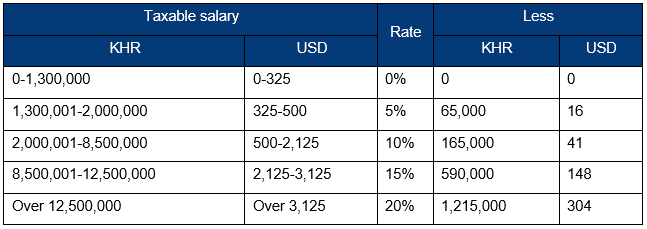

Tax Rate For Resident

(*)Taxable salary and tax rate of resident taxpayer (progressive rate) have been using:

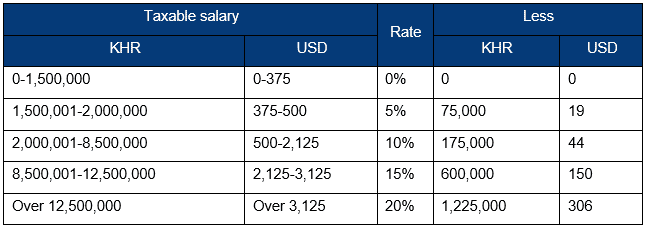

(*)Taxable salary and the tax rate of a resident taxpayer (progressive rate) that will be practiced on 1st January 2023 onwards Pursuant to Sub-Decree of the Royal Government of Cambodia No. 196 dated 28 September 2022:

Tax Rate For Non-Resident

The tax rate for non-residents is a flat rate of 20%. This is a final tax

Rebates On Spouse And Children

The allowance for deduction is KHR150, 000 (USD38) for each dependent:

A housewife supported with marriage certificate,

A child of fewer than 14 years of age; or

A child up to 25 years of age if he/she is a full-time student at an officially recognized educational institution

*Note: this rebate does not apply to the non-resident taxpayer, it’s for resident taxpayers only.

Tax On Fringe Benefits Based

The following payments are subject to tax on fringe benefits:

expenses on entertainment, amusement, or recreation;

educational assistance not part of training program directly related to the performance of the duties of the employee;

schooling fee for employee’s children;

Flight ticket for personal trip;

low-interest loans or Sales below market;

life and health insurance premiums unless the same benefits are provided to all employees regardless of employment position;

contribution to a pension plan in excess of 10% of the employee’s monthly salary exclusive of fringe benefits;

Tax Rate On Fringe Benefits

According to point No. (VII) above, when providing those benefits to employees, fringe benefits tax is at the fixed rate of 20% to both resident and non-resident taxpayers.

other services instead

Using Invoices

Medium and large taxpayers must keep invoices for at least 10 years, and small taxpayers are at least 3 years.

Accommodation Tax (ACCT)

Accommodation Tax is a monthly tax that is imposed on the supply of accommodation services at a rate of 2% of the taxable value inclusive of all taxes except ACCT and VAT.