Withholding tax is imposed on the income of the recipient of the payment, while a payer is obligated to withhold and remit it to the tax authority. It is due when the expense is paid or recorded in the accounting records of the payer.

Residency And Non-Residency

*A Cambodian resident taxpayer includes any physical person who:

has a residence in Cambodia;

has a principal place of abode in Cambodia; or

is physically present in Cambodia for more than 182 days in any 12-month period ending in the current tax year.

*A non-resident for tax purposes is any person who is not a resident in contrast with the above criteria

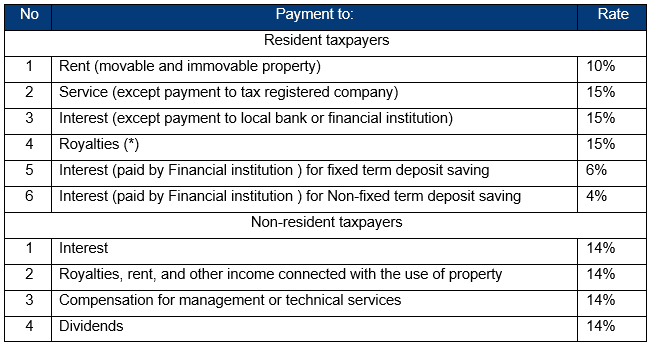

Withholding Tax Rate

Below are the types and rates of withholding tax:

Withholding Tax Exemption

The following transactions is not subject to withholding tax:

Payment for service with an amount lesser than KHR50, 000

Payment for the rental of movable and immovable property to self-declaration taxpayer

Payment in cash or in kind made to a self-declaration taxpayer for the performance of service including management, consulting and other similar services.

Payment in cash or in kind made to a self-declaration taxpayer for the purchase of shrink-wrap software, site license, downloadable software and software bundled with computer hardware.

Expenses paid to state institutions

Salary and fringe benefit expenses paid to staff/ employees

Purchasing goods/ products

Rent (movable and immovable owned by state).

other services instead

Using Invoices

Medium and large taxpayers must keep invoices for at least 10 years, and small taxpayers are at least 3 years.

Accommodation Tax (ACCT)

Accommodation Tax is a monthly tax that is imposed on the supply of accommodation services at a rate of 2% of the taxable value inclusive of all taxes except ACCT and VAT.